The Private Credit Showdown - Traditional Vs Tokenized

Jason Dussault

Chief Executive Officer, Co-Founder

This Post is disseminated on behalf of Intellistake Technologies Corp.

After the 2008 financial crisis, new banking regulations forced traditional lenders to step back from middle-market businesses. Non-bank lenders filled the gap. Investment funds, specialty finance companies, and asset managers started lending directly to private companies. These loans aren't traded on open markets. They're negotiated, held to maturity, and mostly invisible to everyday investors. That's private credit.

Today it's a $3 trillion market.¹ Morgan Stanley projects $5 trillion by 2029.1 But the infrastructure behind it hasn't kept pace with the money flowing into it.

The appeal is straightforward. Potential higher yields than public markets. Floating rate protection when interest rates move. Senior secured positions that put lenders first if something goes wrong.

But There Are Real Problems

For all its growth, private credit still runs on old infrastructure.

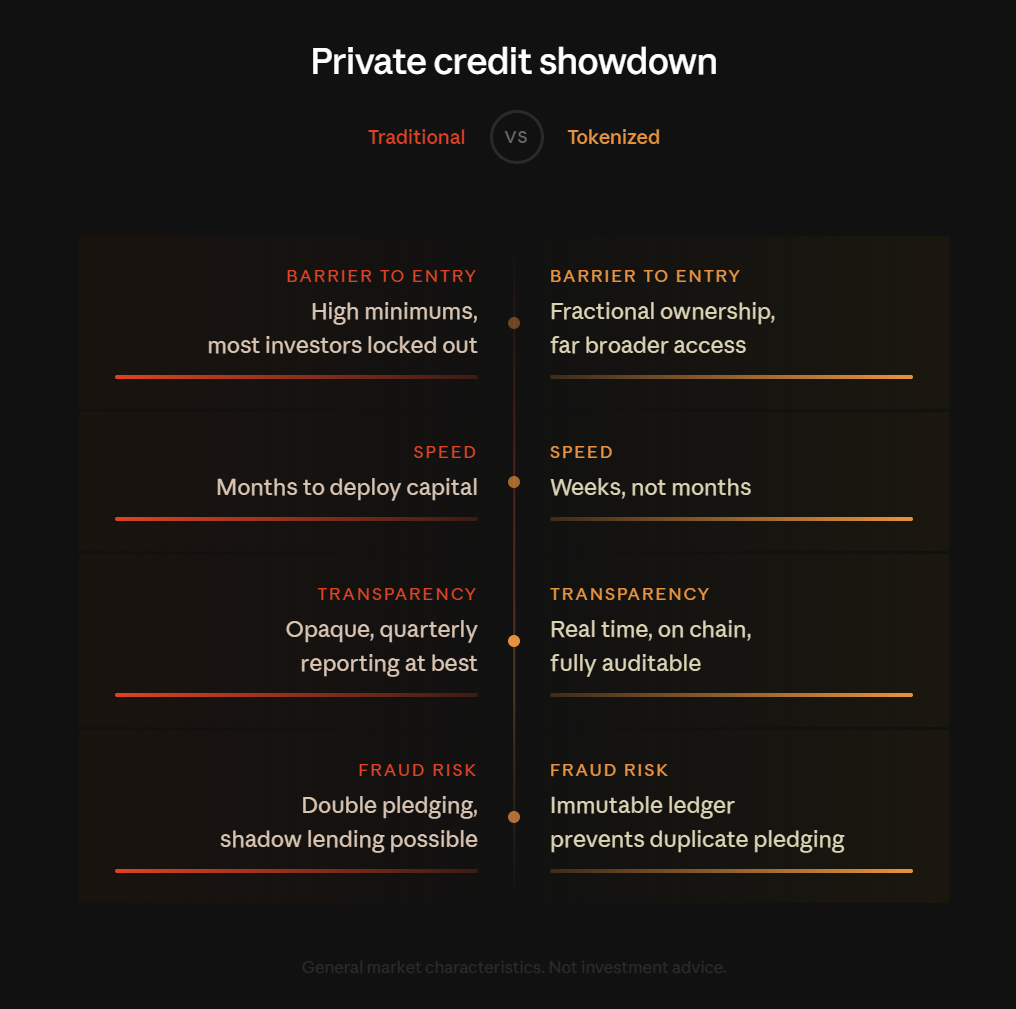

Investments are locked until maturity and there's no real exit. Reporting happens quarterly at best. It's bilateral and opaque, meaning investors don't always know what's actually going on under the hood. Minimum investments usually start at $1 million or more, which keeps most people out entirely. And the day-to-day operations, everything from onboarding to compliance to interest payments, still rely on manual processes and legacy systems.

Recent high-profile collapses have shown what these weaknesses can lead to. In 2025 alone, multiple private credit failures involved allegations of double pledged collateral, fabricated invoices, and billions in assets that couldn't be accounted for. In some cases, banks, auditors, and ratings agencies missed the warning signs for years. Fund gatings left investors locked in with no exit.

These are symptoms of what happens when a market this size is built on systems that rely on trust instead of verification.

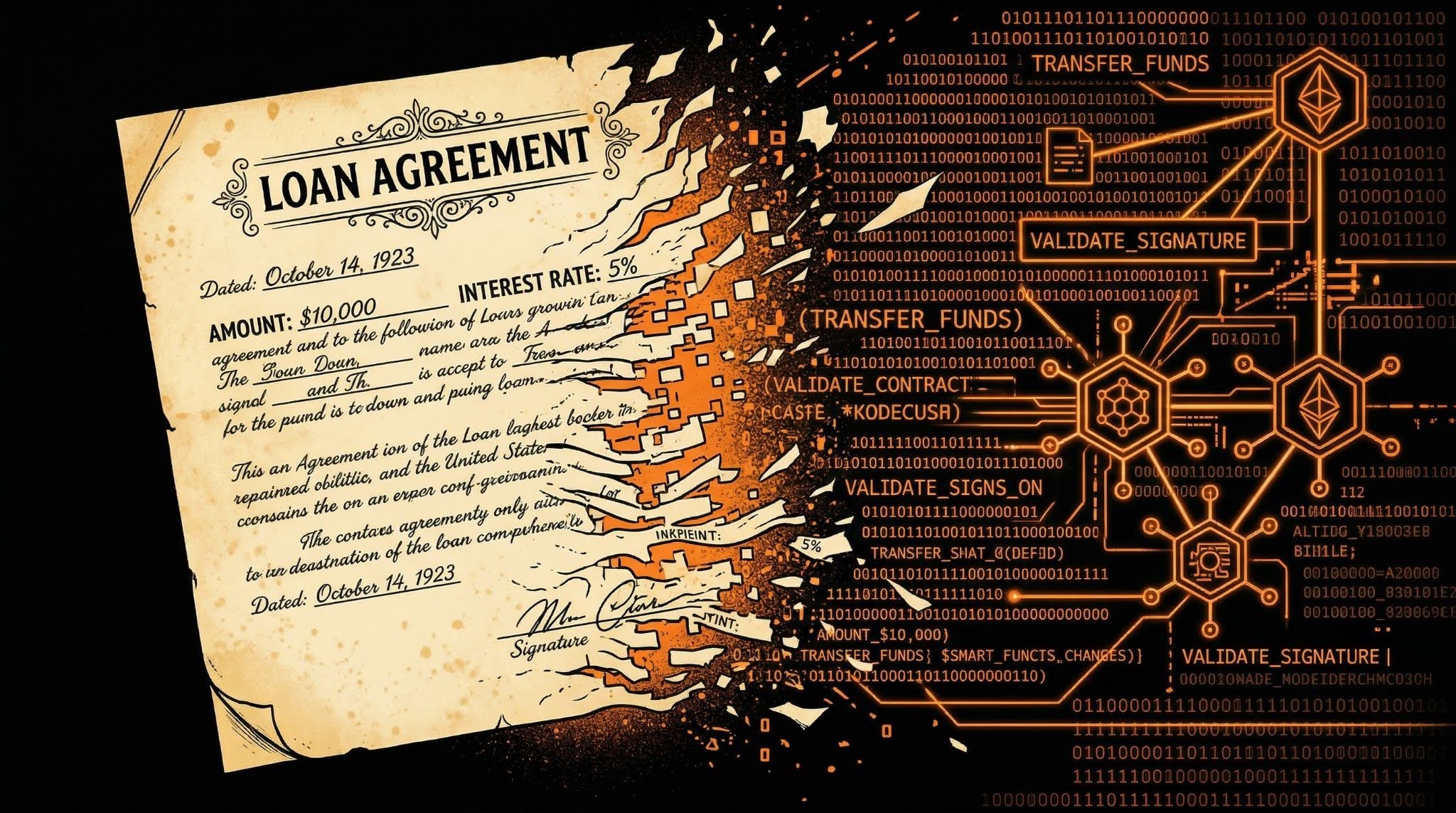

So What Is Tokenized Private Credit?

It takes the same loan or credit exposure and puts the ownership record on a blockchain. The loan itself doesn't change. The legal structure stays the same. The regulation stays the same.

The SEC confirmed in January 2026 that:

“The format in which a security is issued or the methods by which holders are recorded (e.g., onchain vs. offchain) does not affect application of the federal securities laws.” 2

What changes is how it's issued, tracked, settled, and traded.

Smart contracts handle compliance, interest payments, and reporting automatically. Token standards build investor eligibility rules right into the asset, so only verified, eligible investors can hold or trade it. And because it all sits on an immutable ledger, the same collateral can't be pledged to more than one party. That's exactly the type of fraud that took down the recent high-profile collapses.

Settlement happens near instantly instead of waiting through T+1 cycles. Investors can see loan performance continuously rather than waiting for quarterly reports. And the cost savings are real.

Private credit is the biggest category in the tokenized real world asset (RWA) market, making up over $18 billion of the $36 billion total as of January 2026, based on data from rwa.xyz.3 Making up around 50% of the entire tokenized RWA market. That's bigger than tokenized treasuries, commodities, and equities.

But here's what I think matters most. That $18 billion is still only about 0.6% of the $3 trillion traditional market. There's a lot of room to run.

How the Two Stack Up

The Big Players Are Already In

BlackRock now manages nearly $150 billion in assets connected to digital markets, including the world's largest tokenized fund.4 In his 2026 annual letter, CEO Larry Fink proposed replacing the traditional 60/40 portfolio split with a new 50/30/20 model that includes private assets.5 That's a significant statement from the head of the world's largest asset manager.

JPMorgan’s Kinexys platform has already processed over $1.5 trillion in notional value to date.⁶ Meanwhile, both the NYSE and Nasdaq are building dedicated platforms for trading tokenized securities, as momentum continues to build across the sector. A joint BCG and Ripple report projects that the broader tokenized asset market could reach $18.9 trillion by 2033.⁷

The line between traditional finance and tokenized finance is getting thinner. Private credit is already the biggest tokenized asset category by a wide margin. The economics of the asset class haven't changed. The yields are the same, the credit structures are the same, the regulatory frameworks are the same. The infrastructure underneath it is just finally catching up. And the biggest names in finance are the ones building it.

Disclaimer

There has been significant volatility in digital assets and their value can decline rapidly, which in turn would lead to a decline in the stock price of companies holding digital assets. Intellistake is a start-up that does not have the same access to capital as other larger more established companies.

Intellistake has just commenced operating its business and is at an early stage of development. Intellistake is entering this space by acquiring and operating blockchain validator hardware that supports AI networks and investing in AI-related digital tokens to primarily operate validator hardware.

Intellistake is presently evaluating the regulatory framework for tokenization. Any tokenization will be subject to it being completed in compliance with applicable law, regulatory requirements and terms of any underlying agreements associated with the underlying assets. The actual structure of such tokenization, the assets that would be subject to tokenization, and the associated timeline, have not yet been determined. Intellistake will provide further updates as material developments related to this tokenization strategy occur.

Intellistake is developing custom AI software systems called "AI Agents" for businesses. It recently announced the development of IntelliScope, a newly designed enterprise artificial-intelligence (AI) suite that applies decentralized AI technologies to deliver transparent and verifiable corporate intelligence. IntelliScope, which is in testing, is being publicly introduced as Intellistake's enterprise AI suite, reflecting the Company's focus on advancing practical applications of decentralized AI technologies.

The IntelliScope suite is being developed as a collection of modular AI agents, each intended to address specific enterprise challenges. Development has advanced through internal closed testing, where functionality is being refined and validated. Built to leverage decentralized AI technologies developed within the ASI Alliance FET token ecosystem, IntelliScope is now preparing to move into closed beta testing with an enterprise client, a phase focused on gathering feedback to shape premium features and expand real-world use cases.

The Company intends to deliver these solutions either as one-time projects or ongoing subscription services. Revenue is expected to come from implementation fees and monthly subscription payments. The Company does not presently have any customers. Intellistake is just commencing operations. It is targeting significant growth but its business is subject to several risks related to general business, economic and social uncertainties; the sufficiency of cash to meet liquidity needs; legislative, political and competitive developments; the inherent risks involved in the digital currency and general securities markets; the volatility of digital currency prices and the additional risks identified in the "Risk Factors" section of the Company’s filings with applicable securities regulators. Intellistake has not yet developed or commercialized its AI solutions.

Completion of the Singularity Venture Hub (“SVH”) acquisition remains subject to completion of satisfactory due diligence, the negotiation, and execution of a definitive agreement ("Definitive Agreement") that will include representations, warranties, covenants, indemnities, termination rights, and other provisions customary for a transaction of this nature, no objection from the Canadian Securities Exchange, and shareholder approval of SVH, if required.

This report contains "forward-looking information" concerning anticipated developments and events related to the Company that may occur in the future. Forward looking information contained in this report includes, but is not limited to, all statements in respect of the Company's growth and development, the operations and business segments of the Company, support for decentralized AI and blockchain networks, the details of the collaboration with Orbit AI and its expected benefits; the Company’s contributions towards the collaboration with Orbit AI; the timelines for Orbit AI’s operation; and Intellistake’s strategy to support tokenized, decentralized AI infrastructure.

In certain cases, forward-looking information can be identified by the use of words such as "expects", "intends", "anticipates" or variations of such words and phrases or state that certain actions, events or results "may", "would", or "might" suggesting future outcomes, or other expectations, assumptions, intentions or statements about future events or performance. Forward-looking information contained in this report is based on certain assumptions regarding, among other things, the Company and SVH satisfy all conditions necessary to close the proposed transaction; the Company will continue to have access to financing until it achieves profitability; obtaining the necessary regulatory approvals; the technology and blockchain industries in which the Company intends to focus its business in will grow at the rate and in the manner expected; the ability to attract qualified personnel; the success of market initiatives and the ability to grow brand awareness; the ability to distribute Company's services; the Company creates strategies to mitigate risks associated with cryptocurrency price fluctuations; the Company and SVH remain compliant with all applicable laws and securities regulations and applicable licensing requirements; the Company engages and collaborates with local experts, as necessary, to address jurisdiction-specific matters and ensures compliance with foreign regulations to avoid penalties; the Company addresses any potential cybersecurity threats promptly and effectively; the ability of the Company to develop its technology, acquire customers and have revenue; the ability to successfully deploy the new business strategy as a result of the change of business. While the Company considers these assumptions to be reasonable, they may be incorrect.

Forward looking information involves known and unknown risks, uncertainties and other factors which may cause the actual results to be materially different from any future results expressed by the forward-looking information. Such factors include risks related to general business, economic and social uncertainties; failure of the Company and SVH to satisfy all conditions necessary to close the proposed transaction; failure to raise the capital necessary to fund its operations; inability to create strategies to mitigate the risks associated with cryptocurrency price fluctuations; the costs of regulation in the digital asset industries increase to the extent that the Company is no longer generating sufficient returns for shareholders; failure to promptly and effectively address cybersecurity threats; insufficient resources to maintain its operations on a competitive basis; and the actual costs, timing and future plans differs expectations; legislative, environmental and other judicial, regulatory, political and competitive developments; the inherent risks involved in the cryptocurrency and general securities markets; the Company may not be able to profitably liquidate its current digital currency inventory, or at all; a decline in digital currency prices may have a significant negative impact on the Company's operations; the Company's success may depend on the continued involvement of key personnel, including advisors, whose involvement cannot be guaranteed; institutional adoption of decentralized AI infrastructure remains uncertain and may not occur at the pace or scale anticipated; evolving regulatory frameworks, including those related to AI (such as Canada's proposed Artificial Intelligence and Data Act), may impose additional compliance burdens or restrict certain business activities; valuation figures are based on publicly available market data and internal assessments at the time of the referenced transactions and may not reflect current or future valuations; the volatility of digital currency prices; the inherent uncertainty of cost estimates and the potential for unexpected costs and expenses, currency fluctuations; regulatory restrictions, liability, competition, loss of key employees and other related risks and uncertainties; delay or failure to receive regulatory approvals; failure to attract qualified personnel, labour disputes; and the additional risks identified in the "Risk Factors" section of the Company's filings with applicable Canadian securities regulators.

Although the Company has attempted to identify factors that could cause actual results to differ materially from those described in forward-looking information, there may be other factors that cause results not to be as anticipated. Readers should not place undue reliance on forward-looking information. The forward-looking information is made as of the date of this report. Except as required by applicable securities laws, the Company does not undertake any obligation to publicly update forward-looking information.